The Pro-European Left confronts the EU DebtMath Banksters

#

http://alcuinbramerton.blogspot.com/2015/08/greece-2015-democracy-versus-brussels.html

Alcuin Bramerton Twitter .. Alcuin Bramerton Medium .. #1ab archive

Alcuin Bramerton profile ..... Index of blog contents ..... Home .....#1ab

Picture: IMF & Greece 2015. Christine Lagarde & Euclid Tsakalotos.

...........................................................................

▲ Christine Lagarde (IMF) and Euclid Tsakalotos (Greece) ▲

.........................................

Yanis Varoufakis in conversation with leading academics as Greece's leftist Pro-European Syriza party splinters

27th August 2015

When Yanis Varoufakis was elected to parliament and then named as Greek finance minister in January 2015, he embarked on an extraordinary seven months of negotiations with the country’s creditors and its European partners.

On Sunday 5th July 2015, Greek voters backed his hardline stance in a referendum, with a resounding 62% voting No to the European Union’s ultimatum.

On that night, he resigned, after Prime Minister Alexis Tsipras, fearful of an ugly exit from the EuroZone, decided to go against the popular verdict.

Syriza had earned its moment in history and had thrown it away.

Soon afterwards, the governing party Syriza, splintered and a snap election was called for the 20th September 2015.

When asked about Tsipras’s decision to trigger a snap election, inviting the Greek public to issue their judgement on his time in office, Varoufakis said: "If only that were so! Voters are being asked to endorse Alexis Tsipras’ decision, on the night of their majestic referendum verdict, to overturn it; to turn their courageous No into a capitulation, on the grounds that honouring that verdict would trigger a Grexit."

"This is not the same as calling on the people to pass judgement on a record of steadfast opposition to a failed economic programme doing untold damage to Greece’s social economy. It is rather a plea to voters to endorse him, and his choice to surrender, as a lesser evil."

Q: (Anton Muscatelli; University of Glasgow) Why was Greek Prime Minister Alexis Tsipras persuaded to accept the EU’s pre-conditions around the third bailout discussions despite a decisive referendum victory for the No campaign; and is this the end of the road for the anti-austerity wing of Syriza in Greece?

Varoufakis: Tsipras’ answer is that he was taken aback by official Europe’s determination to punish Greek voters by putting into action German finance minister

Wolfgang Schäuble’s plan to push Greece out of the EuroZone, redenominate Greek bank deposits in a currency that was not even ready, and even ban the use of Euros in Greece.

These threats, independently of whether they were credible or not, did untold damage to the European Union’s image as a community of nations and drove a wedge through the axiom of the EuroZone’s indivisibility.

As you probably have heard, on the night of the referendum,

I disagreed with Tsipras on his assessment of the credibility of these threats and resigned as Finance Minister.

But even if I was wrong on the issue of the credibility of the troika’s threats, my great fear was, and remains, that our party, Syriza, would be torn apart by the decision to implement another self-defeating austerity program of the type that we were elected to challenge. It is now clear that my fears were justified.

Q: (Roy Bailey; University of Essex) Was the surprise referendum of the 5th July 2015 conceived as a threat point for the ongoing bargaining between Greece and its creditors, and has the last year caused you to adjust how you think about Game Theory?

Varoufakis: I shall have to disappoint you Roy. As I wrote in a New York Times op-ed (

here), Game Theory was never relevant. It applies to interactions where motives are exogenous and the point is to work out the optimal bluffing strategies and credible threats, given available information. Our task was different: it was to persuade the 'other' side to change their motivation vis-à-vis Greece.

I represented a small, suffering nation in its sixth straight year of deep recession. Bluffing with our people’s fate would be irresponsible. So I did not. Instead, we outlined that which we thought was a reasonable position, consistent with our creditors’ own interests. And then we stood our ground.

When the troika pushed us into a corner, presenting me with an ultimatum on the 25th June 2015, just before closing Greece’s banking system down, we looked at it carefully and concluded that we had neither a mandate to accept it (given that it was economically non-viable) nor to decline it (and clash with official Europe). Instead we decided to do something terribly radical: to put it to the Greek people to decide.

Lastly, on a theoretical point, the 'threat point' in your question refers to John Nash’s bargaining solution (details

here) which is based on the axiom of non-conflict between the parties. Tragically, we did not have the luxury to make that assumption.

Q: (Cristina Flesher Fominaya; University of Aberdeen)

The dealings between Greece and the EU seemed more like a contest between democracy and the banks, than a negotiation between the EU and a member state. Given the outcome, are there any lessons that you would take from this for other European parties resisting the imperatives of austerity politics?

Varoufakis: Allow me to phrase this differently.

It was a contest between the right of creditors to govern a debtor nation and the democratic right of the said nation’s citizens to be self-governed.

You are quite right that there was never a negotiation between the EU and Greece as a member state of the EU. We were negotiating with the troika of lenders, the International Monetary Fund, the European Central Bank and a wholly weakened European Commission in the context of an informal grouping, the EuroGroup, lacking specific rules, without minutes of the proceedings, and completely under the thumb of one finance minister and the troika of lenders.

Moreover,

the troika was terribly fragmented, with many contradictory agendas in play, the result being that the 'terms of surrender' they imposed upon us were, to say the least, curious: a deal imposed by creditors determined to attach conditions which guarantee that we, the debtor, cannot repay them.

So, the main lesson to be learned from the last few months is that European politics is not even about austerity. Or that, as Nicholas Kaldor wrote in The New Statesman in 1971 (commentary

here),

any attempt to construct a monetary union before a political union ends up with a terrible monetary system that makes political union much, much harder. Austerity and a hideous democratic deficit are mere symptoms.

Q: (Panicos Demetriades; University of Leicester) Did you ever think that your message was being diluted or becoming noisy, or even incoherent, by giving so many interviews?

Varoufakis: Yes. I have regretted several interviews, especially when the journalists involved took liberties that I had not anticipated. But let me also add that the 'noise' would have prevailed even if I granted far fewer interviews. Indeed

the media game was fixed against our government, and me personally, in the most unexpected and repulsive way.

Wholly moderate and technically sophisticated proposals were ignored, while the media concentrated on trivia and distortions. Giving interviews where I would, to some extent, control the content was my only outlet. Faced with an intentionally 'noisy' media agenda that bordered on character assassination, I erred on the side of over-exposure.

Q: (Simon Wren-Lewis; University of Oxford) Might it have been possible for a forceful France to have provided an effective counterweight to Germany in the EuroGroup, or did Germany always have a majority on its side?

Varoufakis:

The French government feels that it has a weak hand.

Its deficit is persistently within the territory of the so-called

excessive deficit procedure of the European Commission, which puts Pierre Moscovici, the European commissioner for economic and financial affairs, and France’s previous finance minister, in the difficult position of having to act tough on Paris under the watchful eye of Wolfgang Schäuble, the German finance minister.

It is also true, as you say, that

the EuroGroup is completely 'stitched up' by Schäuble. Nevertheless, France had an opportunity to use the Greek crisis in order to change the rules of a game that France will never win. The French government has, thus, missed a major opportunity to render itself sustainable within the single currency.

The result, I fear, is that Paris will soon be facing a harsher régime, possibly a situation where the president of the EuroGroup is vested with draconian veto powers over the French government’s national budget. How long, once this happens, can the European Union survive the resurgence of nasty nationalism in places like France?

Q: (Kamal Munir; University of Cambridge) You often implied that what went on in your meetings with the troika (the IMF, ECB and European Commission) was economics only on the surface. Deep down, it was a political game being played. Don’t you think we are doing a disservice to our students by teaching them a brand of economics that is so clearly detached from this reality?

Varoufakis: If only some economics were to surface in our meetings with the troika, I would be happy! None did. Even when economic variables were discussed, there was never any economic analysis.

The discussions were exhausted at the level of rules and agreed targets. I found myself talking at cross-purposes with my interlocutors. They would say things like: “The rules on the primary surplus specify that yours should be at least 3.5% of GDP in the medium term.” I would try to have an economic discussion suggesting that this rule ought to be amended because, for example, the 3.5% primary target for 2018 would depress growth today, boost the debt-to-GDP ratio immediately and make it impossible to achieve the said target by 2018.

Such basic economic arguments were treated like insults. Once I was accused of 'lecturing' them on macroeconomics.

On your pedagogical question: while it is true that

we teach students a brand of economics that is designed to be blind to really-existing capitalism, the fact remains that no type of sophisticated economic thinking, not even neoclassical economics, can reach the parts of the EuroGroup which make momentous decisions behind closed doors.

Q: (Mariana Mazzucato; University of Sussex) How has the crisis in Greece (its cause and its effects) revealed failings of neoclassical economic theory at both the micro and the macro level?

Varoufakis: The uninitiated may be startled to hear that

the macroeconomic models taught at the best universities feature no accumulated debt, no involuntary unemployment and, indeed, no money (with relative prices reflecting a form of barter).

Save perhaps for a few random shocks that demand and supply are assumed to quickly iron out, the snazziest models taught to the brightest of students assume that savings automatically turn into productive investment, leaving no room for crises.

It makes it hard when these graduates come face-to-face with reality. They are at a loss, for example, when they see German savings that permanently outweigh German investment, while Greek investment outweighs savings during the 'good times' (before 2008) but collapses to zero during the crisis.

Moving to the micro level, the observation that, in the case of Greece, real wages fell by 40% but employment dropped precipitously, while exports remained flat, illustrates in Technicolor

how useless a microeconomics approach bereft of macro foundations truly is.

Q: (Tim Bale; Queen Mary University of London) Do you see any similarities between yourself and Jeremy Corbyn, who looks like he might win the UK Labour leadership, and do you think a left-wing populist party is capable of winning an election under a first-past-the-post system?

Varoufakis: The similarity that I feel at liberty to mention is that Corbyn and I, probably, coincided at many demonstrations against the Tory government while I lived in Britain in the 1970s and 1980s, and share many views regarding the calamity that befell working Britons as power shifted from manufacturing to finance. However, all other comparisons must be kept in check.

Syriza was a radical party of the Left that scored a little more than 4% of the vote in 2009. Our incredible rise was due to the collapse of the political 'centre' caused by popular discontent at a Great Depression due to a single currency that was never designed to sustain a global crisis, and by the denial of the powers-that-be that this was so.

The much greater flexibility that the Bank of England afforded to Gordon Brown’s and David Cameron’s British governments prevented the type of socio-economic implosion that led Syriza to power and, in this sense, a similarly buoyant radical left party is most unlikely in Britain. Indeed, the Labour Party’s own history, and internal dynamic, will, I am sure, constrain a victorious Jeremy Corbyn in a manner alien to Syriza.

Turning to the first-past-the-post system, had it applied here in Greece, it would have given our party a crushing majority in parliament. It is, therefore, untrue that Labour’s electoral failures are due to this system.

Lastly, allow me to urge caution with the word 'populist'.

Syriza did not put to Greek voters a populist agenda. 'Populists' try to be all things to all people. Our promised benefits extended only to those earning less than £500 per month. If it wants to be popular, Labour cannot afford to be populist either.

Q: (Mark Taylor; University of Warwick) Would you agree that Greece does not fulfil the criteria for successful membership of a currency union with the rest of Europe? Wouldn’t it be better if they left now rather than simply papering over the cracks and waiting for another Greek economic crisis to occur in a few years’ time?

Varoufakis:

The EuroZone’s design was such that even France and Italy could not thrive within it. Under the current institutional design

only a currency union east of the Rhine and north of the Alps would be sustainable. Alas, it would constitute a union useless to Germany, as it would fail to protect it from constant revaluation in response to its trade surpluses.

Now, if by 'criteria' you meant

the Maastricht limits, it is of course clear that Greece did not fulfil them. But then again nor did Italy or Belgium.

Conversely, Spain and Ireland did meet the criteria and, indeed, by 2007 the Madrid and Dublin governments were registering deficit, debt and inflation numbers that, according to the official criteria, were better than Germany’s. And yet when the crisis hit, Spain and Ireland sunk into the mire.

In short,

the EuroZone was badly designed for everyone. Not just for Greece.

So should we cut our losses and get out? To answer properly we need to grasp the difference between saying that Greece, and other countries, should not have entered the EuroZone, and saying now that we should now exit. Put technically, we have a case of hysteresis: once a nation has taken the path into the EuroZone, that path disappeared after the Euro’s creation and any attempt to reverse along that, now non-existent, path could lead to a great fall off a tall cliff.

The original text and packaging of this Q&A is

here (27.08.15).

.........................................

Picture: Debt or credit which cannot be paid back is never an asset.

Picture: Greece EU referendum. Greferendum. Athens 5th July 2015. Cartoon 1.

Picture: Greece EU referendum. Greferendum. Athens 5th July 2015. Cartoon 3.

Picture: Greece EU referendum. Greferendum. Athens 5th July 2015. Cartoon 5.

Picture: Greece. Greferendum. When debt is fraudulent .... debt forgiveness.

Picture: Greece. Greferendum. No. Tsipras. Merkel. Hollande. Juncker.

#

Greece has been, and still is, the victim of an attack premeditated and organised by the International Monetary Fund, the European Central Bank, and the European Commission. This violent, illegal, and immoral mission was aimed exclusively at shifting private debt on to the public sector.

Truth Committee on the Greek Public Debt

Executive Summary

17th June 2015

In June 2015 Greece stands at a crossroad of choosing between furthering the failed macroeconomic adjustment programmes imposed by the creditors or making a real change to break the chains of debt.

Five years since the economic adjustment programmes began, the country remains deeply cemented in an economic, social, democratic and ecological crisis.

The black box of debt has remained closed, and until now no authority, Greek or international, has sought to bring to light the truth about how and why Greece was subjected to the Troika régime. The debt, in whose name nothing has been spared, remains the rule through which neoliberal adjustment is imposed, and the deepest and longest recession experienced in Europe during peacetime.

There is an immediate need and social responsibility to address a range of legal, social and economic issues that demand proper consideration. In response, the Hellenic Parliament established the Truth Committee on Public Debt in April 2015, mandating the investigation into the creation and growth of public debt, the way and reasons for which debt was contracted, and the impact that the conditionalities attached to the loans have had on the economy and the population.

The Truth Committee has a mandate to raise awareness of issues pertaining to the Greek debt, both domestically and internationally, and to formulate arguments and options concerning the cancellation of the debt.

The research of the Committee presented in this preliminary report sheds light on the fact that the entire adjustment programme, to which Greece has been subjugated, was and remains a politically orientated programme. The technical exercise surrounding macroeconomic variables and debt projections, figures directly relating to people’s lives and livelihoods, has enabled discussions around the debt to remain at a technical level mainly revolving around the argument that the policies imposed on Greece will improve its capacity to pay the debt back. The facts presented in this report challenge this argument.

All the evidence we present in this report shows that

Greece not only does not have the ability to pay this debt, but also should not pay this debt first and foremost because the debt emerging from the Troika’s arrangements is a direct infringement on the fundamental human rights of the residents of Greece. Hence, we came to the conclusion that

Greece should not pay this debt because it is illegal, illegitimate, and odious.

It has also come to the understanding of the Committee that the unsustainability of the Greek public debt was evident from the outset to the international creditors, the Greek authorities, and the corporate media. Yet,

the Greek authorities, together with some other governments in the EU, conspired against the restructuring of public debt in 2010 in order to protect financial institutions. The corporate media hid the truth from the public by depicting a situation in which the bailout was argued to benefit Greece, whilst spinning a narrative intended to portray the population as deservers of their own wrongdoings.

Bailout funds provided in both programmes of 2010 and 2012 have been externally managed through complicated schemes, preventing any fiscal autonomy. The use of the bailout money is strictly dictated by the creditors, and so, it is revealing that less than 10% of these funds have been destined to the government’s current expenditure.

This preliminary report presents a primary mapping out of the key problems and issues associated with the public debt, and notes key

legal violations associated with the contracting of the debt; it also traces out the legal foundations, on which unilateral suspension of the debt payments can be based. The findings are presented in nine chapters structured as follows:

Chapter 1, Debt before the Troika, analyses the growth of the Greek public debt since the 1980s. It concludes that the increase in debt was not due to excessive public spending, which in fact remained lower than the public spending of other Eurozone countries, but rather due to the

payment of extremely high rates of interest to creditors, excessive and unjustified military spending, loss of tax revenues due to illicit capital outflows, state recapitalisation of private banks, and the international imbalances created via the flaws in the design of the Monetary Union itself.

Adopting the Euro led to a drastic increase of private debt in Greece to which major European private banks as well as the Greek banks were exposed. A growing banking crisis contributed to the Greek sovereign debt crisis. George Papandreou’s government helped to present the elements of a banking crisis as a sovereign debt crisis in 2009 by emphasizing and boosting the public deficit and debt.

Chapter 2, Evolution of Greek public debt during 2010-2015, concludes that the first loan agreement of 2010, (was) aimed primarily to rescue the Greek and other European private banks, and to allow the banks to reduce their exposure to Greek government bonds.

Chapter 3, Greek public debt by creditor in 2015, presents the contentious nature of Greece’s current debt, delineating the loans’ key characteristics, which are further analysed in Chapter 8.

Chapter 4, Debt System Mechanism in Greece reveals the mechanisms devised by the agreements that were implemented since May 2010. They created a substantial amount of new debt to bilateral creditors and the European Financial Stability Fund (EFSF), whilst generating

abusive costs thus deepening the crisis further. The mechanisms disclose how

the majority of borrowed funds were transferred directly to financial institutions. Rather than benefitting Greece, they have accelerated the privatization process, through the use of financial instruments.

Chapter 5, Conditionalities against sustainability, presents how the

creditors imposed intrusive conditionalities attached to the loan agreements, which led directly to the economic unviability and unsustainability of debt. These conditionalities, on which the creditors still insist, have not only contributed to lower GDP as well as higher public borrowing, hence a higher public debt/GDP making Greece’s debt more unsustainable, but also engineered dramatic changes in the society, and caused a humanitarian crisis.

The Greek public debt can be considered as totally unsustainable at present.

Chapter 6, Impact of the “bailout programmes” on human rights, concludes that the measures implemented under the “bailout programmes” have directly affected living conditions of the people and violated human rights, which Greece and its partners are obliged to respect, protect and promote under domestic, regional and international law.

The drastic adjustments, imposed on the Greek economy and society as a whole, have brought about a rapid deterioration of living standards, and remain incompatible with social justice, social cohesion, democracy and human rights.

Chapter 7, Legal issues surrounding the MOU and Loan Agreements, argues

there has been a breach of human rights obligations on the part of Greece itself and the lenders, that is the Euro Area (Lender) Member States, the European Commission, the European Central Bank, and the International Monetary Fund, who imposed these measures on Greece. All these actors failed to assess the human rights violations as an outcome of the policies they obliged Greece to pursue, and also directly

violated the Greek constitution by effectively stripping Greece of most of its sovereign rights.

The agreements contain abusive clauses, effectively

coercing Greece to surrender significant aspects of its sovereignty. This is imprinted in the choice of the English law as governing law for those agreements, which facilitated the circumvention of the Greek Constitution and international human rights obligations.

Conflicts with human rights and customary obligations, several indications of contracting parties acting in bad faith, which together with the unconscionable character of the agreements, render these agreements invalid.

Chapter 8, Assessment of the Debts as regards illegitimacy, odiousness, illegality, and unsustainability, provides an assessment of the Greek public debt according to the definitions regarding illegitimate, odious, illegal, and unsustainable debt adopted by the Committee.

Chapter 8 concludes that the Greek public debt as of June 2015 is unsustainable, since Greece is currently unable to service its debt without seriously impairing its capacity to fulfill its basic human rights obligations. Furthermore,

for each creditor, the report provides evidence of indicative cases of illegal, illegitimate and odious debts.

Debt to the IMF should be considered illegal since its concession breached the IMF’s own statutes, and its conditions breached the Greek Constitution, international customary law, and treaties to which Greece is a party. It is also illegitimate, since conditions included policy prescriptions that infringed human rights obligations. Finally, it is odious since the IMF knew that the imposed measures were undemocratic, ineffective, and would lead to serious violations of socio-economic rights.

Debts to the ECB should be considered illegal since the ECB over-stepped its mandate by imposing the application of macroeconomic adjustment programs (e.g. labour market deregulation) via its participation in the Troïka. Debts to the ECB are also illegitimate and odious, since the principal raison d’etre of the Securities Market Programme (SMP) was to serve the interests of the financial institutions, allowing the major European and Greek private banks to dispose of their Greek bonds.

The EFSF engages in cash-less loans which should be considered illegal because Article 122(2) of the Treaty on the Functioning of the European Union (TFEU) was violated, and further they breach several socio-economic rights and civil liberties. Moreover, the EFSF Framework Agreement 2010 and the Master Financial Assistance Agreement of 2012 contain

several abusive clauses revealing clear misconduct on the part of the lender. The EFSF also acts against democratic principles, rendering these particular debts illegitimate and odious.

The bilateral loans should be considered illegal since they violate the procedure provided by the Greek constitution. The loans involved clear misconduct by the lenders, and had conditions that contravened law or public policy.

Both EU law and international law were breached in order to sideline human rights in the design of the macroeconomic programmes.

The bilateral loans are furthermore illegitimate, since they were not used for the benefit of the population, but merely enabled the private creditors of Greece to be bailed out. Finally, the bilateral loans are odious since the lender states and the European Commission knew of potential violations, but in 2010 and 2012 avoided to assess the human rights impacts of the macroeconomic adjustment and fiscal consolidation that were the conditions for the loans.

The debt to private creditors should be considered illegal because private banks conducted themselves irresponsibly before the Troika came into being, failing to observe due diligence, while some private creditors such as hedge funds also acted in bad faith.

Parts of the debts to private banks and hedge funds are illegitimate for the same reasons that they are illegal; furthermore, Greek banks were illegitimately recapitalized by tax-payers.

Debts to private banks and hedge funds are odious, since major private creditors were aware that these debts were not incurred in the best interests of the population but rather for their own benefit.

The report comes to a close with some practical considerations.

Chapter 9, Legal foundations for repudiation and suspension of the Greek sovereign debt, presents the

options concerning the cancellation of debt, and especially the conditions under which a sovereign state can exercise the right to unilateral act of repudiation or suspension of the payment of debt under international law.

Several legal arguments permit a State to unilaterally repudiate its illegal, odious, and illegitimate debt. In the Greek case, such a unilateral act may be based on the following arguments:

the bad faith of the creditors that pushed Greece to violate national law and international obligations related to human rights; preeminence of human rights over agreements such as those signed by previous governments with creditors or the Troika; coercion; unfair terms flagrantly violating Greek sovereignty and violating the Constitution; and finally,

the right recognised in international law for a State to take countermeasures against illegal acts by its creditors, which purposefully damage its fiscal sovereignty, oblige it to assume odious, illegal and illegitimate debt, violate economic self-determination and fundamental human rights.

As far as unsustainable debt is concerned,

every state is legally entitled to invoke necessity in exceptional situations in order to safeguard those essential interests threatened by a grave and imminent peril. In such a situation, the State may be dispensed from the fulfilment of those international obligations that augment the peril, as is the case with outstanding loan contracts. Finally,

states have the right to declare themselves unilaterally insolvent where the servicing of their debt is unsustainable, in which case they commit no wrongful act and hence bear no liability.

People’s dignity is worth more than illegal, illegitimate, odious and unsustainable debt

Having concluded a preliminary investigation, the Committee considers that

Greece has been and still is the victim of an attack premeditated and organised by the International Monetary Fund, the European Central Bank, and the European Commission. This violent, illegal, and immoral mission aimed exclusively at shifting private debt onto the public sector.

Making this preliminary report available to the Greek authorities and the Greek people, the Committee considers to have fulfilled the first part of its mission as defined in the decision of the President of Parliament of 4 April 2015.

The Committee hopes that the report will be a useful tool for those who want to exit

the destructive logic of austerity and stand up for what is endangered today: human rights, democracy, peoples’ dignity, and the future of generations to come.

In response to those who impose unjust measures, the Greek people might invoke what Thucydides mentioned about the constitution of the Athenian people: "As for the name,

it is called a democracy, for the administration is run with a view to the interests of the many, not of the few” (Pericles’ Funeral Oration, in the speech from Thucydides’ History of the Peloponnesian War).

Source of Executive Summary here (17.06.15). Full report here (18.06.15 - pdf 64pp).

#

Picture: Greece versus Europe 2015. Tsipras. Varoufakis. Merkel. Putin.

#

The Prime Minister of Greece, Alexis Tsipras:

The EU, of which Greece is a member, must rediscover its true course by returning to its founding statutory principles and declarations: Solidarity, democracy, social justice. This will be impossible, though, if the EU persists with austerity policies and the disruption of social cohesion, which only serve to further the recession.

Let us not fool ourselves: the so-called Greek problem is not a Greek problem. It is a European problem.

The problem is not Greece. The problem is the EuroZone, and its very structure.

And the question remains, whether the EU will allow room for growth, social cohesion and prosperity. Whether it will allow room for political solidarity, instead of policies imposing dead ends and failed projects.

Source here.

The Greek government submitted specific proposals concerning the social security system’s reorganisation. We agreed to the immediate abolition of the early retirement option that increases the average retirement age, and we are committed to moving forward immediately with the consolidation of the pension funds, thus reducing their operating expenses and restricting special arrangements.

As we analysed in detail during our discussions with the institutions, these reforms function decisively in favor of the sustainability of the system. And like all reforms, their results will not be apparent from one day to another.

Sustainability requires a long-term perspective and cannot be subject to narrow, short-term fiscal criteria (e.g. reducing expenditure by 1% of GDP in 2016).

Benjamin Disraeli used to say that there are three kinds of lies: lies, damned lies and statistics. Let us not allow an obsessive-compulsive use of indices to destroy the comprehensive agreement that we prepared over the previous period of intensive negotiations. The duty rests on all of our shoulders.

Source here.

The Finance Minister of Greece, Yanis Varoufakis:

Last Thursday’s EuroGroup meeting (18th June 2015) went down in history as a lost opportunity to produce an already belated agreement between Greece and its creditors.

The EuroZone moves in a mysterious way.

Momentous decisions are rubber- stamped by finance ministers who remain in the dark on the details, while unelected officials of mighty institutions are locked into one-sided negotiations with a solitary government-in-distress.

It is as if Europe has determined that elected finance ministers are not up to the task of mastering the technical details; a task best left to “experts” representing not voters but the institutions.

One can only wonder to what extent such an arrangement is efficient, let alone remotely democratic.

What Greece now needs desperately is serious, proper reforms. We need

a new tax system that helps defeat evasion and curtail political or corporate interference,

a corruption-free procurement system, business-friendly licensing procedures, judicial reforms, elimination of scandalous early retirement practices, proper regulation of the media and of political party finances.

Source here.

The only antidote to propaganda and malicious ‘leaks’ is transparency. After so much disinformation on my presentation at the EuroGroup of the Greek government’s position, the only response is to post the precise words uttered within. Read them and judge for yourselves whether the Greek government’s proposals constitute a basis for agreement.

Five months have gone by, the end of the road is nigh, but this finely balancing act has failed to materialise. Yes, at the Brussels Group we have come close. How close? On the fiscal side the positions are truly close, especially for 2015. For 2016 the remaining gap amounts to 0.5% of GDP. We have proposed parametric measures of 2% versus the 2.5% that the institutions insist upon. This 0.5% gap we propose to bridge over by administrative measures.

It would be a major error to allow such a minuscule difference to cause massive damage to the Eurozone’s integrity. Convergence had also been achieved on a wide range of issues.

At this, the 11th hour, stage of the negotiations,

before uncontrollable events take over, we have a moral duty, let alone a political and an economic one, to overcome this impasse. This is no time for recriminations and accusations. European citizens will hold collectively responsible all those of us who failed to strike a viable solution.

Source here.

What were the causes of the Euro Crisis? News media and politicians love simple stories. Like Hollywood, they adore morality tales featuring villains and victims. Aesop’s fable of the Ant and the Grasshopper proved an instant hit.

From 2010 onwards the story goes something like this: The Greek grasshoppers did not do their homework and their debt-fuelled summer one day ended abruptly. The ants were then called upon to bail them out. Now, the German people are being told, the Greek grasshoppers do not want to pay their debt back. They want another bout of loose living, more fun in the sun, and another bailout so that they can finance it.

It is a powerful story. A story underpinning the tough stance that many advocate against the Greeks, against our government. The problem is that

it is a misleading story. A story that casts a long shadow on the truth. An allegory that is turning one proud nation against another. With losers everywhere. Except perhaps

the enemies of Europe and of democracy who are having a field day.

To maintain a nation’s trade surpluses within a monetary union the banking system must pile up increasing debts upon the deficit nations. Yes, the Greek state was an irresponsible borrower. But

for every irresponsible borrower, there corresponds an irresponsible lender. Take Ireland or Spain and contrast it with Greece. Their governments, unlike ours, were not irresponsible. But then the Irish and the Spanish private sectors ended up taking up the extra debt that their government did not. Total debt in the Periphery was the reflection of the surpluses of the Northern, surplus nations.

This is why

there is no profit to be had from thinking about debt in moral terms. We built an asymmetrical monetary union with rules that guaranteed the generation of unsustainable debt. This is how we built it. We are all responsible for it. Jointly. Collectively. As Europeans. And we are all responsible for fixing it.

Source here.

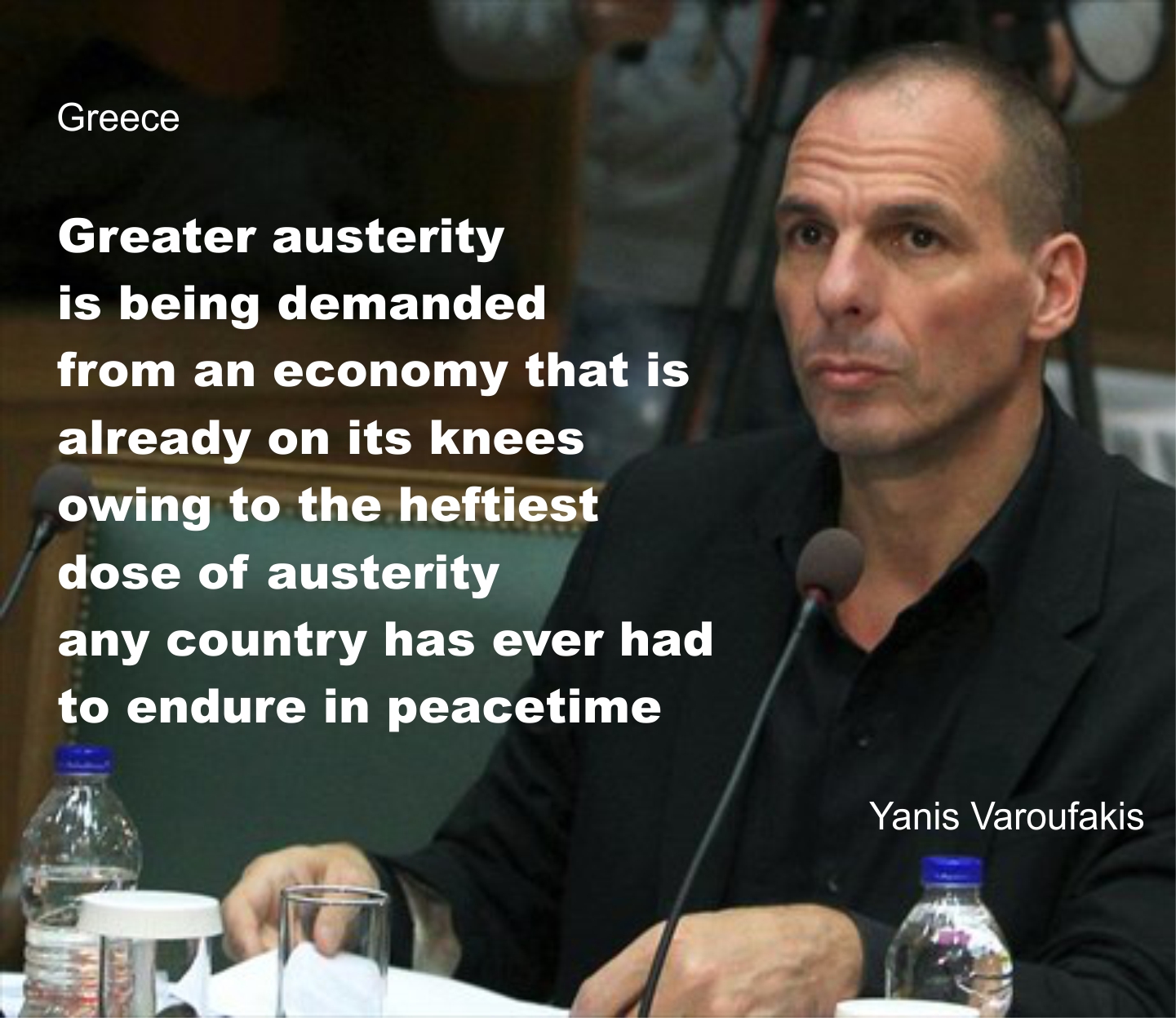

Picture: Athens, Greece. Everlasting austerity.Yanis Varoufakis.

On Friday 6th September 1946, the US Secretary of State,

James F. Byrnes, travelled to Stuttgart to deliver his historic

Speech of Hope.

Byrnes’ address marked America’s post-war change of heart vis-à-vis Germany, and gave a fallen nation a chance to imagine recovery, growth, and a return to normalcy. Seven decades later, it is my country, Greece, that needs such a chance.

Until Byrnes’

Speech of Hope, the Allies were committed to converting “…Germany into a country primarily agricultural and pastoral in character.” That was the express intention of the Morgenthau Plan, devised by US Treasury Secretary, Henry Morgenthau Jnr, and co-signed by the United States and Britain two years earlier, in September 1944.

Indeed, when the US, the Soviet Union, and the United Kingdom signed the

Potsdam Agreement in August 1945, they agreed on the “reduction or destruction of all civilian heavy-industry with war potential” and on “restructuring the German economy toward agriculture and light industry.”

By 1946, the Allies had reduced Germany’s steel output to 75% of its pre-war level. Car production plummeted to around 10% of pre-war output. By the end of the decade, 706 industrial plants were destroyed.

Byrnes’ speech signalled to the German people a reversal of that punitive de-industrialization drive.

Of course, Germany owes its post-war recovery and wealth to its people and their hard work, innovation, and devotion to a united, democratic Europe. But Germans could not have staged their magnificent post-war renaissance without the support signified by the

Speech of Hope.

Prior to Byrnes’ speech, and for a while afterwards, America’s allies were not keen to restore hope to the defeated Germans. But once President Harry Truman’s administration decided to rehabilitate Germany, there was no turning back. Its rebirth was underway, facilitated by the Marshall Plan, the US-sponsored 1953 debt write-down, and by the infusion of migrant labor from Italy, Yugoslavia, and Greece.

Europe could not have united in peace and democracy without that sea change.

Someone had to put aside moralistic objections and look dispassionately at a country locked in

a set of circumstances that would only reproduce discord and fragmentation across the continent. The US, having emerged from the war as the only creditor country, did precisely that.

Today, it is my country that is locked in such circumstances and in need of hope. Moralistic objections to helping Greece abound, denying its people a shot at achieving their own renaissance.

Greater austerity is being demanded from an economy that is on its knees, owing to the heftiest dose of austerity any country has ever had to endure in peacetime. No offer of debt relief. No plan for boosting investment. And certainly, as of yet, no

Speech of Hope for this fallen people.

It is the mark of ancient societies, like those of Germany and of Greece, that

contemporary tribulations revive old fears and foment new discord. So we must be careful. Teenagers should never be told that, due to some 'prodigal sin', they deserve to be educated in cash-strapped schools and weighed down by mass unemployment, whether the scene is Germany in the late 1940s or Greece today.

As I write these lines, the Greek government is presenting the European Union with a set of proposals for deep reforms, debt management, and an investment plan to kick-start the economy. Greece is indeed ready and willing to enter into a compact with Europe that will eliminate the deformities that caused it to be the first domino to fall in 2010.

But, if Greece is to implement these reforms successfully, its citizens need a missing ingredient: Hope. A

Speech of Hope for Greece would make all the difference now - not only for us, but also for our creditors, as

our renaissance would terminate the default risk.

What should such a declaration include? Just as Byrnes’ address was short on detail but long on symbolism, a

Speech of Hope for Greece does not have to be technical. It should simply mark a sea change,

a break with the past five years of adding new loans on top of already unsustainable debt, conditional on further doses of punitive austerity.

Who should deliver it? In my mind, the speaker should be German Chancellor Angela Merkel, addressing an audience in Athens or Thessaloniki, or any Greek city of her choice. She could use the opportunity to hint at a new approach to European integration: one that starts in the country that has suffered the most,

a victim both of the EuroZone’s faulty monetary design and of its society’s own failings.

Hope was a force for good in post-war Europe, and it can be a force for positive transformation now. A speech by Germany’s leader in a Greek city could go a long way toward delivering it.

The original text of this piece by the Greek Finance Minister, Yanis Varoukafis, can be found at Project Syndicate here (04.06.15).

Picture: Greece. PM Alexis Tsipras. May 2015. Athens. EU.

#

Europe is at a crossroads.

The issue of Greece does not only concern Greece; it is at the very epicentre of a conflict between two diametrically opposing strategies concerning the future of European unification.

Alexis Tsipras

On 25th January 2015, the Greek people made a courageous decision. They dared to challenge the one-way street of the Memorandum’s tough austerity, and to seek a new agreement. A new agreement that will keep the country in the Euro, with a viable economic program, without the mistakes of the past.

The Greek people paid a high price for these mistakes; over the past five years

the unemployment rate climbed to 28% (60% for young people), average income decreased by 40%, while according to Eurostat’s data, Greece became the EU country with the highest index of social inequality.

And the worst result: Despite badly damaging the social fabric, this Program failed to invigorate the competitiveness of the Greek economy.

Public debt soared from 124% to 180% of GDP, and despite the heavy sacrifices of the people, the Greek economy remains trapped in continuous uncertainty caused by unattainable fiscal balance targets that further the vicious cycle of austerity and recession.

The new Greek government’s main goal during these last four months has been to put an end to this vicious cycle, an end to this uncertainty.

Doing so requires a mutually beneficial agreement that will set realistic goals regarding surpluses, while also reinstating an agenda of growth and investment. A final solution to the Greek problem is now more mature and more necessary than ever.

Such an agreement will also spell the end of the European economic crisis that began 7 years ago, by putting an end to the cycle of uncertainty in the Eurozone.

Today,

Europe has the opportunity to make decisions that will trigger a rapid recovery of the Greek and European economy by ending Grexit scenarios, scenarios that prevent the long-term stabilization of the European economy and may, at any given time, weaken the confidence of both citizens and investors in our common currency.

Many, however, claim that the Greek side is not cooperating to reach an agreement because it comes to the negotiations intransigent and without proposals.

Is this really the case?

Because

these times are critical, perhaps historic - not only for the future of Greece but also for the future of Europe - I would like to take this opportunity to present the truth, and to responsibly inform the world’s public opinion about the real intentions and positions of Greece.

The Greek government, on the basis of the Eurogroup’s decision on February 20th, has submitted a broad package of reform proposals, with the intent to reach an agreement that will combine respect for the mandate of the Greek people with respect for the rules and decisions governing the Eurozone.

One of the key aspects of our proposals is the commitment to lower - and hence make feasible - primary surpluses for 2015 and 2016, and to allow for higher primary surpluses for the following years, as we expect a proportional increase in the growth rates of the Greek economy.

Another equally fundamental aspect of our proposals is the commitment to increase public revenues through

a redistribution of the burden from lower and middle classes to the higher ones that have effectively avoided paying their fair share to help tackle the crisis, since they were for all accounts protected by both the political élite and the Troika who turned 'a blind eye'.

From the very start, our government has clearly demonstrated its intention and determination to address these matters by

legislating a specific bill to deal with fraud caused by triangular transactions, and by intensifying customs and tax controls to reduce smuggling and tax evasion.

While, for the first time in years, we charged media owners for their outstanding debts owed to the Greek public sector.

These actions are changing things in Greece, as evidenced by the speeding up of work in the courts to administer justice in cases of substantial tax evasion. In other words,

the oligarchs who were used to being protected by the political system now have many reasons to lose sleep.

In addition to these overarching goals that define our proposals, we have also offered highly detailed and specific plans during the course of our discussions with the institutions that have bridged the distance between our respective positions that separated us a few months ago.

Specifically, the Greek side has accepted to implement a series of institutional reforms, such as strengthening the independence of the General Secretariat for Public Revenues and of the Hellenic Statistical Authority (ELSTAT), interventions to accelerate the administration of justice, as well as interventions in the product markets to eliminate distortions and privileges.

Also, despite our clear opposition to the privatization model promoted by the institutions that neither creates growth perspectives nor transfers funds to the real economy and the unsustainable debt, we accepted to move forward, with some minor modifications, on privatizations to prove our intention of taking steps towards approaching the other side.

We also agreed to implement a major VAT reform by simplifying the system and reinforcing the redistributive dimension of the tax in order to achieve an increase in both collection and revenues.

We have submitted specific proposals concerning measures that will result in a further increase in revenues. These include

a special contribution tax on very high profits, a tax on e-betting, the intensification of checks of bank account holders with large sums - tax evaders, measures for the collection of public sector arrears, a special luxury tax, and a tendering process for broadcasting and other licenses, which the Troika coincidentally forgot about for the past five years.

These measures will increase revenues, and will do so without having recessionary effects since they do not further reduce active demand or place more burdens on the low and middle social strata.

Furthermore, we agreed to implement a major reform of the social security system that entails integrating pension funds and repealing provisions that wrongly allow for early retirement, which increases the real retirement age.

These reforms will be put into place despite the fact that the losses endured by the pension funds, which have created the medium-term problem of their sustainability, are mainly due to political choices of both the previous Greek governments and especially the Troika, who share the responsibility for these losses:

the pension funds’ reserves have been reduced by 25 billion through the PSI and from very high unemployment, which is almost exclusively due to the extreme austerity program that has been implemented in Greece since 2010.

Finally - and despite our commitment to the workforce to

immediately restore European legitimacy to the labor market that has been fully dismantled during the last five years under the pretext of competitiveness - we have accepted to implement labour reforms after our consultation with the ILO, which has already expressed a positive opinion about the Greek government’s proposals.

Given the above, it is only reasonable to wonder why there is such insistence by Institutional officials that Greece is not submitting proposals.

What end is served by this prolonged liquidity moratorium towards the Greek economy? Especially in light of the fact that Greece has shown that it wants to meet its external obligations, having paid more than 17 billion in interest and amortizations (about 10% of its GDP) since August 2014 without any external funding.

And finally,

what is the purpose of the coordinated leaks that claim that we are not close to an agreement that will put an end to the European and global economic and political uncertainty fueled by the Greek issue?

The informal response that some are making is that we are not close to an agreement because the Greek side insists on its positions to restore collective bargaining and refuses to implement a further reduction of pensions.

Here, too, I must make some clarifications:

Regarding the issue of collective bargaining, the position of the Greek side is that it is impossible for the legislation protecting employees in Greece to not meet European standards or, even worse, to flagrantly violate European labor legislation.

What we are asking for is nothing more than what is common practice in all Eurozone countries. This is the reason why I recently made a joint declaration on the issue with President Juncker.

Concerning the issue on pensions, the position of the Greek government is completely substantiated and reasonable.

In Greece, pensions have cumulatively declined from 20% to 48% during the Memorandum years; currently 44.5% of pensioners receive a pension under the fixed threshold of relative poverty while approximately 23.1% of pensioners, according to data from Eurostat, live in danger of poverty and social exclusion.

It is therefore obvious that

these numbers, which are the result of Memorandum policy, cannot be tolerated - not simply in Greece but in any civilized country.

So, let’s be clear:

The lack of an agreement so far is not due to the supposed intransigent, uncompromising and incomprehensible Greek stance. It is due to the insistence of certain institutional actors on submitting absurd proposals and displaying a total indifference to the recent democratic choice of the Greek people, despite the public admission of the three Institutions that necessary flexibility will be provided in order to respect the popular verdict.

What is driving this insistence?

An initial thought would be that

this insistence is due to the desire of some to not admit their mistakes and instead, to reaffirm their choices by ignoring their failures.

Moreover, we must not forget the public admission made a few years ago by the IMF that they erred in calculating the depth of the recession that would be caused by the Memorandum.

I consider this, however, to be a shallow approach.

I simply cannot believe that the future of Europe depends on the stubbornness or the insistence of some individuals.

My conclusion, therefore, is that

the issue of Greece does not only concern Greece; rather, it is the very epicentre of conflict between two diametrically opposing strategies concerning the future of European unification.

The first strategy aims to deepen European unification in the context of equality and solidarity between its people and citizens.

The proponents of this strategy begin with the assumption that it is not possible to demand that the new Greek government follows the course of the previous one - which, we must not forget, failed miserably. This assumption is the starting point, because otherwise, elections would need to be abolished in those countries that are in a Program. Namely, we would have to accept that the institutions should appoint the Ministers and Prime Ministers, and that citizens should be deprived of the right to vote until the completion of the Program.

In other words,

this means the complete abolition of democracy in Europe, the end of every pretext of democracy, and the beginning of disintegration and of an unacceptable division of United Europe.

This means the beginning of

the creation of a technocratic monstrosity that will lead to a Europe entirely alien to its founding principles.

The second strategy seeks precisely this: The split and the division of the Eurozone, and consequently of the EU.

The first step to accomplishing this is to create a two-speed Eurozone where the 'core' will set tough rules regarding austerity and adaptation and will appoint a 'super' Finance Minister of the EZ with unlimited power, and with the ability to even reject budgets of sovereign states that are not aligned with

the doctrines of extreme neoliberalism.

For those countries that refuse to bow to the new authority, the solution will be simple: Harsh punishment. Mandatory austerity. And even worse, more restrictions on the movement of capital, disciplinary sanctions, fines and even a parallel currency.

Judging from the present circumstances,

it appears that this new European power is being constructed, with Greece being the first victim. To some, this represents a golden opportunity to make an example out of Greece for other countries that might be thinking of not following this new line of discipline.

What is not being taken into account is the high amount of risk and the enormous dangers involved in this second strategy.

This strategy not only risks the beginning of the end for the European unification project by shifting the Eurozone from a monetary union to an exchange rate zone, but it also triggers economic and political uncertainty, which is likely to entirely transform the economic and political balances throughout the West.

Europe, therefore, is at a crossroads. Following the serious concessions made by the Greek government, the decision is now not in the hands of the institutions, which in any case - with the exception of the European Commission - are not elected and are not accountable to the people, but rather in the hands of Europe’s leaders.

Which strategy will prevail? The one that calls for a Europe of solidarity, equality and democracy, or the one that calls for rupture and division?

If some, however, think or want to believe that this decision concerns only Greece, they are making a grave mistake. I would suggest that they re-read Hemingway’s masterpiece, “For Whom the Bell Tolls”.

The original English translation of this piece by Alexis Tsipras is

here. It first appeared in the Le Monde newspaper (Paris) on Sunday 31st May 2015.

Picture: Greece. Alexis Tsipras. May 2015. Athens. Greece. EU.

Picture: Yanis Varoufakis. May 2015. Athens. Greece. EU.

Picture: Zoe Konstantopoulou. May 2015. Athens. Greece. EU.

Picture: Zoe Konstantopoulou of Syriza. Wednesday 20th May 2015. Athens.

Picture: EuroZone breakup? New Drachma notes. Old Deutsche Mark notes.

Picture: Greece: Until 2015, an unholy alliance between oligarchs & politicians?

#

Blue for you: Athens and the power of weakness

Has Syriza just become the most powerful political entity in the Western world?

Greece's vast debts to international institutions and zombiebanks mean that the Syriza government in Athens is now more powerful than the IMF, the ECB & the G7 banking cartel put together.

Debt or credit which cannot be paid back is never an asset; it is always a liability. And when much of that debt has been fraudulently imposed, debt forgiveness is the logical and only remedy.

The Nazi-continuum money laundries at the ECB and the US Fed, and the puppet-politicians they control, all know that one false move on their part, in dealing with the Syriza leaders, will bring the whole Western fiat finance system down like a sharpster's house of cards.

The house of cards is currently kept standing by covert rigging of the Western financial markets into a counterintuitive bull mode. Any major, unmanageable, surprise shock to do with sovereign debt or default, given the transparent oxygen of publicity, will turn bull into bear. The bond bubble will burst. It's all about the bonds. When that bubble bursts, the old world ends.

One of the reasons Germany is so nervous about Greece is that Frankfurt's Deutsche Bank is staring down the last abyss. Insiders say it has a massive overhang of out-of-the-money, cross-collateralised derivatives hiding on its books, off-ledger. Any sharp word from Athens about non-payment of a strategically positioned visible debt might bring the bank down. The UK financial community knows the risk. Deutsche Bank was kicked out of the London Gold Fix syndicate in May 2014.

Notwithstanding 2008 and all that, several US & EU banks are still quietly using mortgage-backed securities as collateral in derivatives trades.

In the G7 fiat finance system, about $100 trillion of bonds are in play. Most of these are also pledged as collateral for derivatives. So, at a conservative estimate, because of the leveraging involved, the downside risk attached to the G7's bonds is about $555 trillion. This is ten times greater than the downside risk in the CDS market in 2008. And, according to the story told, a single bank failure brought that lot down very quickly.

The G7 bankers' worst nightmare is on the cusp of manifesting. How many Western banks hold Greek sovereign bonds as collateral for out-of-the-money, cross-collateralised derivatives? Quite a few, it would appear. Why else has the G7 banking cartel been so eager to hedge its books with stolen pension funds used as collateral?

The global sovereign bond index is flashing alarms. Between late March and early June 2015, it lost $625 billion.

The potential chances for catastrophic Western wealth destruction at short notice are very real. More

here.

In Greece, Syriza knows all this. The Syriza finance & economics people may be useless at, and impatient with, vested-interest oligarch politics, but in terms of pure pragmatic economics they are brighter, brainier and freer than the frightened people across the table from them in Europe. And they have nothing to lose. Anything of value which Greece once had has already been lost to externally-imposed, everlasting austerity.

Syriza has also been talking to Vladimir Putin. He has told them how the world works. They have learned that it is a game of chess. And in a game of chess, sometimes it's the waiting move which kills. Slow the clock down and threaten stalemate.

On a chessboard, sometimes you win, not by piling energy into a dynamic situation faster than your opponent can think, but by withdrawing energy to the point of excruciating boredom. Your apparent inactivity obliges your opponent to kick the can down the road yet again. The clock ticks. Stuff happens. Jam tomorrow.

On other occasions, however, a gambit may gain a telling advantage. Several quite big gambits are prepared in Athens.

The

White Spiritual Boy issue, concerning the fraudulent start-up funding of the Euro currency from off-ledger, black screen accounts in the late 1990s, has been referenced elsewhere on this blog. It has to do with putative titles to Asian gold and the Nazi-continuum

Committee of 300's Black Book of banking codes. This is a powerful piece on the board. It is only a pawn, still. But it is on the seventh rank and is well-defended. More

here.

On Thursday 7th May 2015, the Russian President, Vladimir Putin, had a telephone conversation with Alexis Tsipras, the Prime Minister of Greece. Putin said that Moscow was willing to provide financing to Greek companies involved in constructing the GreekStream link to the TurkStream gas pipeline. This will carry Russian gas into Europe.

On Friday 8th May 2015, an American

DC corporation apparatchik called Amos J. Hochstein (US State Department) arrived in Athens to talk to Panagiotis Lafazanis, the Greek Energy Minister. But he was a day late. The board had changed. More

here and

here.

Also in play on the same board is a knight, enthusiastic about German World War II reparations due to Greece. The idea here is simple: the total amount of reasonably audited war reparations as yet unpaid by Germany to Greece is close to, or a little more than, Greece's total national debt. The war

reparations due have been calculated at €280 - €340 billion (source

here). Greece's total national debt is between €332 & €345 billion (depending upon what you call debt and how you do the sums).

Athens can therefore quite reasonably say to its creditors: "OK, we'll pay off all our debts to you, but not until Germany has paid off all its war reparations to us. Deal?"

Until recently, this potential move was being reported as a baseless fantasy by the Western mainstream media. But then two things happened. First, Russia got on the phone again. Moscow could help Greece in its investigation into possible Second World War reparations from Germany by providing access to previously unused archives. A list of the relevant Russian records, including documents, photographs and documentary footage was duly passed to Athens. More

here.

Second, something much more public happened within the Greek capital itself. Large screens all across the Athens metro, usually reserved for weather forecasts, began to loop video footage of the Nazi occupation of Greece in World War Two. It was a government-backed video demanding German war reparations. More

here.

A day or two later, on Sunday 10th May 2015, the German Chancellor, Angela Merkel, was in Russia to lay a wreath at the Grave of the Unknown Soldier in Moscow, and to talk with Vladimir Putin. She wasn't a happy bunny. She wasn't supposed to be. Look at the official Kremlin-circulated

picture of the meeting. A man's got to do what a man's got to do. And these days, in Northern Hemisphere geopolitics outside China, most of the real men are in Moscow, Tehran and Athens.

On Thursday 14th May 2015, in Athens, the place to be was the Athenaeum

InterContinental Hotel. The Greek Finance Minister, Yanis Varoufakis,

was speaking at an Economist Conference called the

19th Roundtable with the Government of Greece.

Varoufakis was straightforward and honest: “I wish we (still) had the

Drachma; I wish we had never entered this (European) monetary union. And

I think that deep down all member states with the EuroZone would agree

with that now. Because it was very badly constructed. But once you are

in, you don’t get out without a catastrophe.”

During his address, Varoufakis referred to the idea that the ECB’s

SMP-program Greek government (pre-2012) bonds (face value €27B) could be

repaid through the ESM, with a parallel swap between new Greek

government bonds and the ESM. But he warned that such a bond swap,

designed to ease Athens’ cash-crunch, was likely to be rejected, because

it struck "fear into the soul" of the European Central Bank president,

Mario Draghi. However, Varoufakis stressed that whatever other stratagem

might be proposed by Europe and the IMF, the Greek government would not

sign up to any bailout plan that would send Greece into a “death

spiral”. More

here and

here.

As if on cue, later that afternoon, Moscow reported a pertinent

development in the Russian media. On the previous Monday, the 11th May

2015, Greece's ruling party, Syriza, had published a statement saying

that Russia had invited Greece to become the sixth member of the BRICS

New Development Bank, joining Brazil, Russia, India, China and South

Africa in that initiative.

The invitation was made by the Russian Deputy Finance Minister, Sergei

Storchak, during a telephone conversation with the Greek Prime Minister,

Alexis Tsipras. According to the Syriza statement, Tsipras received the

proposal with interest and promised to consider it thoroughly. Subsequently, an unnamed Greek government source told Sputnik News (Moscow) that Tsipras would

have an opportunity to discuss potential Greek accession to the bank

with the leaders of the BRICS group in Saint Petersburg next month, where he is scheduled to participate in a high-level Economic Forum on the

18th to 20th June.

"It was a pleasant surprise," the Greek source said, noting that

Greece’s foreign policy is very diversified. "We are members of the

European Union and of the EuroZone, but at the same time we acknowledge

that there are also other powers in the world, and we will make our

decisions taking into account our own interests, while fulfilling the

commitments we have in other international organisations we are part

of." More

here.

On the World War II reparations issue, a further development was

articulated inside Germany. On Saturday 16th May 2015, in a piece in Der

Spiegel magazine, Dieter Deiseroth, a senior judge at Germany’s Supreme

Administrative Court, offered a legal perspective.

He said that Greece’s demand that Germany pays back a loan the country

was forced to give under Nazi occupation during WW2, is just. The loan

in question is now worth €11 billion. Greece should appeal to the

International Court of Justice at The Hague, if it wants to claim the

loan. This would require the agreement of Berlin or, alternatively, the

agreement of the OSCE’s Court of Conciliation and Arbitration.

Deiseroth went on to say that the request for individual war

compensation for Greek victims could also be granted. There cannot be a

limitation period for Greece's claims as a result of the Two Plus Four

Agreement. 2+4 is a classic example of an agreement against a third

party.

“Greece has not waived its demands.” Just because the claim(s) have

never been expressed in writing, does not negate Greece's case. "There’s

no waver through silence.” More

here and

here.

In Athens, one of the Syriza MPs is

Zoe Konstantopoulou. She is the

speaker of the Greek parliament. Konstantopoulou, a Sorbonne-educated

human rights lawyer, has set up a Debt Truth committee in her office.

In addition to overseeing Greece's WWII reparation claims, she is taking

on Germany in another way. There is a slew of élite corruption cases

focussing on dodgy Greek public sector contracts with German firms. Some

of these, it now appears, may have been signed under unlawful duress

earlier in the EuroZone crisis.

Konstantopoulou's committee has also identified other apparently

fraudulent papers. These concern coercive loans pressed on, and accepted

by, other Greek administrations since 2008. One particular tranche of

Greek debt has been described as 'unconstitutional'.

Konstantopoulou comments: “There is strong evidence of the illegitimacy,

odiousness and unsustainability of a large part of what is purported to

be the Greek public debt.” She has been warning Greece's creditors that

the Greek people have the right to demand the writing-off of the part

which is not owed.

“Pending the audit, it is unethical on the part of creditors to demand

further payments, while refusing disbursements and, at the same time,

exercising extortionate pressure for the implementation of policies

contrary to the public mandate. More

here.

With regard to The Doctrine of Odious Debts, and the developing debate

about Transnational Debt Forgiveness, we have summarised the core

principles on another blog page

here.

Until Greece, and now Ukraine, came along, these issues were thought in

the West to be tribal salon discussions confined to Africa and South

America. As such, they could be easily managed by a handful of

accurately-deployed bribes and a few unexplained car crashes. Whether

these tried and tested remedies will work in Syriza's Athens in 2015

appears to be in doubt.

#

#

Joint statement: Jean-Claude Juncker (EC) and Alexis Tsipras (Greece)

Wednesday 6th May 2015

President Juncker and Prime Minister Tsipras spoke on the phone this morning. They took stock of progress made in the talks between Greece and its partners over the last days on a comprehensive set of reforms to achieve a successful completion of the review.

They notably discussed the importance of reforms to modernise the pension system so that it is fair, fiscally sustainable and effective in

averting old age poverty.

They also discussed the need for wage developments and labour market institutions to be

supportive of job creation, competitiveness and

social cohesion.

In this context, they concurred on the role of a modern and effective collective bargaining system, which should be developed through broad consultation and meet the highest European standards.

Constructive talks should continue within the Brussels Group.

Original text

here (06.05.15).

A Blueprint for Greece’s Recovery - Yanis Varoufakis

Wednesday 6th May 2015

Months of negotiations between our government and the International Monetary Fund, the European Union, and the European Central Bank have produced little progress.

One reason is that

all sides are focusing too much on the strings to be attached to the next liquidity injection and not enough on a vision of how Greece can recover and develop sustainably. If we are to break the current impasse, we must envisage a healthy Greek economy.

Sustainable recovery requires synergistic reforms that unleash the country’s considerable potential by removing bottlenecks in several areas: productive investment,

credit provision, innovation, competition, social security, public administration, the judiciary, the labor market, cultural production, and, last but not least, democratic governance.

Seven years of debt deflation, reinforced by

the expectation of everlasting austerity, have decimated private and public investment and forced anxious, fragile banks to stop lending.

With the government lacking fiscal room, and

Greek banks burdened by non-performing loans, it is important to mobilize the state’s remaining assets and unclog the flow of bank credit to healthy parts of the private sector.

To restore investment and credit to levels consistent with economic escape velocity, a recovering

Greece will require two new public institutions that work side by side with the private sector and with European institutions:

A development bank that harnesses public assets and

a “bad bank” that enables the banking system to get out from under their non-performing assets and restore the flow of credit to profitable, export-oriented firms.

Imagine a development bank levering up collateral that comprises post-privatization equity retained by the state and other assets (for example, real estate) that could easily be made more valuable (and collateralized) by reforming their property rights.

Imagine that it links the European Investment Bank and the European Commission President Jean-Claude Juncker’s €315 billion ($350 billion) investment plan with Greece’s private sector.

Instead of being viewed as a fire sale to fill fiscal holes, privatization would be part of a grand public-private partnership for development.

Imagine further that the “bad bank” helps the financial sector, which was

recapitalized generously by strained Greek taxpayers in the midst of the crisis, to shed their legacy of non-performing loans and unclog their financial plumbing. In concert with the development bank’s virtuous impact, credit and investment flows would flood the Greek economy’s hitherto arid realms, eventually helping the bad bank turn a profit and become “good.”

Finally, imagine the effect of all of this on Greece’s financial, fiscal, and social-security ecosystem:

With bank shares skyrocketing, our state’s losses from their recapitalisation would be extinguished as its equity in them appreciates.

Meanwhile, the development bank’s dividends would be channeled into the long-suffering pension funds, which were abruptly de-capitalized in 2012 (owing to the “haircut” on their holdings of Greek government bonds).

In this scenario, the task of bolstering social security would be completed with the unification of pension funds; the surge of contributions following the pickup in employment; and the return to formal employment of workers banished into informality by

the brutal deregulation of the labour market during the dark years of the recent past.

One can easily imagine Greece recovering strongly as a result of this strategy.

In a world of ultra-low returns, Greece would be seen as a splendid opportunity, sustaining a steady stream of inward foreign direct investment. But why would this be different from the pre-2008 capital inflows that fueled debt-financed growth?

Could another macroeconomic Ponzi scheme really be avoided?

During the era of Ponzi-style growth, capital flows were channeled by commercial banks into a frenzy of consumption, and by the state into

an orgy of suspect procurement and outright profligacy. To ensure that this time is different, Greece will need to reform its social economy and political system.

Creating new bubbles is not our government’s idea of development.

This time, by contrast, the new development bank would take the lead in channeling scarce homegrown resources into selected productive investment. These include startups, IT companies that use local talent, organic-agro small and medium-size enterprises, export-oriented pharmaceutical companies, efforts to attract the international film industry to Greek locations, and educational programs that take advantage of Greek intellectual output and unrivaled historic sites.

In the meantime, Greece’s regulatory authorities would be keeping a watchful eye over commercial lending practices, while a debt brake would prevent our government from indulging in old, bad habits, ensuring that our state never again slips into primary deficits.

Cartels, anti-competitive invoicing practices, senselessly closed professions, and a bureaucracy that has traditionally turned the state into a public menace would soon discover that our government is their worst foe.

The barriers to growth in the past were

an unholy alliance among oligarchic interests and political parties, scandalous procurement, clientelism, the permanently broken media, overly accommodating banks, weak tax authorities, and a weighed-down, fearful judiciary.

Only the bright light of democratic transparency can remove such impediments; our government is determined to help it shine through.

Original text

here (06.05.15).

#

Picture: Has Greece got a lot more hidden money than it thinks?

..........................................................

The US Federal Reserve Money Laundry

Global banking crisis? What global banking crisis?

Universal debt forgiveness and the imminent global debt jubilee

The White Spiritual Boy off-ledger black screen accounts

The World Global Settlement Funds

European bloodlines face end-time vortex of exposure

The JP Morgan Blue Book. The Secret Book of Redemption.

The Future Historians' List

Index of blog contents

#

#

#

.jpg?SSImageQuality=Full)

.jpg?SSImageQuality=Full)

{kind=link}

{kind=link}

{kind=link}

{kind=link}